Trace Elements Market Analysis

I,Analysis of non-ferrous metals

Week-on-week: Month-on-month:

| Units | Week 4 of January | Week 5 of January | Week-on-week changes | December average price | January average price | Month-on-month change | Current price as of February 26 | |

| Shanghai Metals Market # Zinc ingots | Yuan/ton |

24310 |

25082 |

↑772 |

23070 |

24516 |

↑1446 |

24460 |

| Shanghai Metals Network # Electrolytic copper | Yuan/ton |

100525 |

102812 |

↑2287 |

93236 |

102039 |

↑8803 |

101795 |

| Shanghai Metals Network AustraliaMn46% manganese ore | Yuan/ton |

42.15 |

42.15 |

↑0.3 |

41.58 |

42.18 |

↑0.6 |

42.45 |

| The price of imported refined iodine by Business Society | Yuan/ton |

635000 |

635000 |

- |

635000 |

635000 |

- |

635000 |

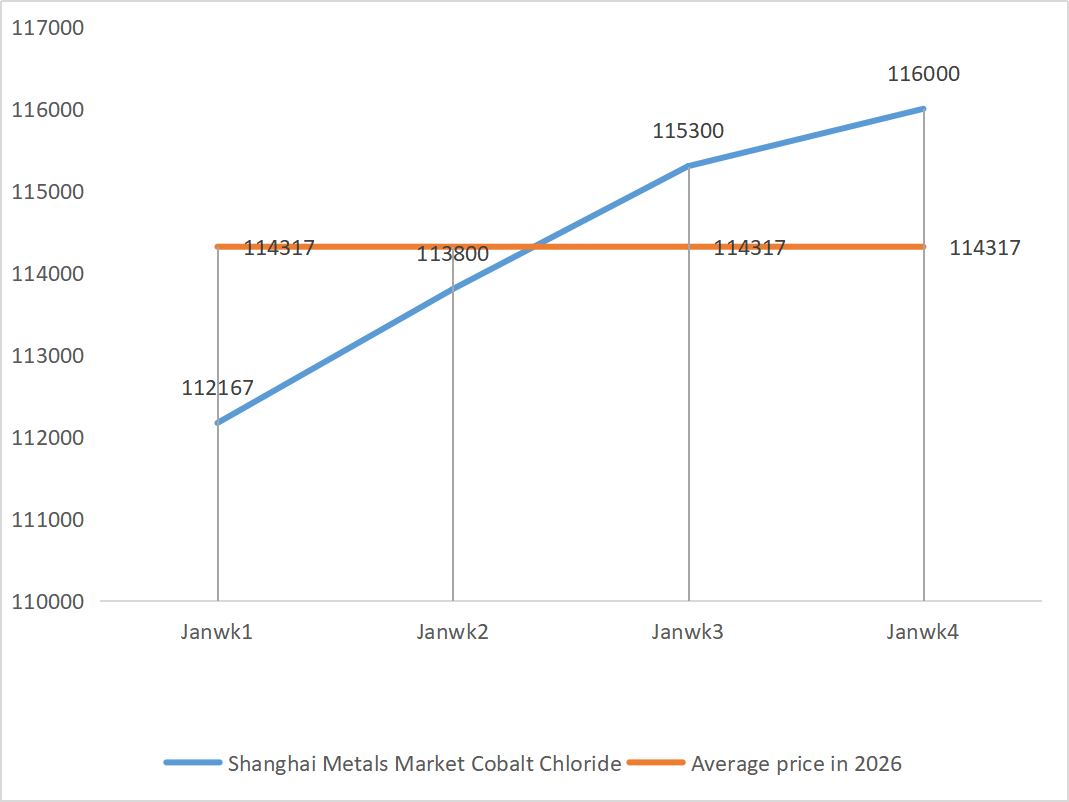

| Shanghai Metals Market Cobalt Chloride(co≥24.2%) | Yuan/ton |

116000 |

116000 |

- |

109135 |

115275 |

↑6140 |

116000 |

| Shanghai Metals Market Selenium Dioxide | Yuan/kilogram |

136.5 |

145.5 |

↑9 |

112.9 |

132.50 |

↑19.6 |

167.5 |

| Capacity utilization rate of titanium dioxide manufacturers | % |

72.86 |

73 |

↑0.14 |

74.69 |

75.2 |

↑0.51 |

1)Zinc sulfate

① Raw materials: Zinc hypooxide: Supply tightness persists and manufacturers’ quotations remain firm.

Zinc network price background: High volatility. Zinc prices rose significantly on the first trading day after the Spring Festival (February 24), but there was a lack of willingness to buy in the spot market, with sluggish market sales and light transactions, coupled with the accumulation of domestic inventories. On the cost side: The import window for zinc ore is closed and domestic northern mines are expected to resume full operations in April-May, and processing fees for zinc ore are expected to remain low at present. In addition, there are disruptions in Iran’s zinc supply, and the cost side provides some support for zinc prices. Macro: Market sentiment is mixed with bulls and bears. On the one hand, Nvidia’s strong earnings reignited AI trading enthusiasm, boosting base metals across the board.

Overall, the current zinc market is in a game between strong expectations (macro and cost support) and weak reality (high inventories, weak consumption). Zinc prices are expected to fluctuate strongly in the short term. It is expected to fluctuate around 24,000-24,800 yuan per ton.

② Sulfuric acid: The current sulfuric acid market, under the combined effect of cost support, tight supply and rigid demand, is showing a stable but slightly strong operation trend. Short-term prices are expected to continue to fluctuate upward

The upstream operating rate of zinc sulfate enterprises is normal, but the order intake is significantly insufficient. The spot market has experienced various levels of pullbacks. Feed enterprises have not been very active in recent purchases. Under the dual pressure of upstream enterprises’ operating rates and insufficient existing orders, zinc sulfate will continue to operate around stability in the short term.

2)Manganese sulfate

Raw materials: ① Strong cost support: The prices of raw materials manganese ore and sulfuric acid remain firm, continuing to support costs.

② Sulfuric acid prices remain high and stable.

Supply side: Mostly production determines sales, operating rates remain high, but some enterprises fluctuate slightly due to factors such as Spring Festival maintenance. Overall supply is relatively stable, but companies have a strong willingness to hold prices due to raw material costs. On the cost side: Manganese ore prices have been consolidating and fluctuating, while sulfuric acid prices remain high. The double pressure of raw material costs has supported manganese sulfate prices to remain at a relatively high level.

It is expected that manganese sulfate prices will remain firm in the short term, but factors such as fluctuations in raw material prices, the recovery of downstream demand, and the progress of enterprise order delivery need to be closely watched. Prices may continue to rise if raw material costs increase further or if downstream demand recovers significantly.

3)Ferrous sulfate

Raw materials: The current ferrous sulfate market is in a tight balance of “supply constraints”. Production cuts in the upstream titanium dioxide industry have led to a contraction in the supply of its by-product ferrous sulfate, which has been diverted by the lithium iron phosphate industry. The operating rate is 80% (up 20% from the previous month), but the capacity utilization rate remains at 25% (up 6% from the previous month), with limited production recovery.

The titanium dioxide industry’s operating rate remains low, the supply of by-products is restricted, and the demand for iron phosphate surges. This supply-demand gap is unlikely to be resolved in the short term. The cost of ferrous sulfate monohydrate producers is rising. Currently, the overall operating rate of ferrous sulfate in China is not good, and enterprises have very little spot inventory, which brings favorable factors for the price increase of ferrous sulfate. Most domestic ferrous enterprises are currently shut down. Considering the recent inventory levels of enterprises and the upstream operating rates, ferrous sulfate is expected to rise in the short term. Customers are advised to increase their inventories appropriately.

4)Copper sulfate/basic copper chloride

Based on recent price data, copper prices show the following characteristics: Price fluctuation features

Range of fluctuations: Recently, copper prices have mainly fluctuated within the range of 99,605 to 104,410 yuan per ton

The latest price: The current 101,795 yuan/ton is at the upper-middle level of the recent price range

Fluctuation range: The maximum fluctuation is about 4,805 yuan/ton, indicating a certain degree of market volatility. Copper sulfate is expected to remain at a high level with volatility in the short term.

Stable supply and demand: On the supply side, the operating rate of domestic copper sulfate producers is relatively stable, and the market supply is relatively sufficient; On the demand side, there have been no significant fluctuations in demand from downstream industries such as electroplating, aquaculture, and chemicals. The overall market supply and demand are basically balanced.

In the short term, the price of copper sulfate is expected to continue to fluctuate within the current range. If copper prices rise further, it could drive up copper sulfate prices slightly. In the long term, as environmental policies become stricter and industry consolidation progresses, the copper sulfate market is expected to gradually move towards high-end and green development, but in the short term, price fluctuations will still be greatly influenced by costs and supply and demand. Customers are advised to keep an eye on copper prices and purchase as needed.

5)Magnesium sulfate/magnesium oxide

In terms of raw materials: Currently, sulfuric acid in the north is stable at a high level.

Magnesium oxide and magnesium sulfate prices have risen. The impact of magnesite resource control, quota restrictions and environmental rectification has led to many enterprises producing based on sales. Light-burned magnesium oxide enterprises shut down on Friday due to capacity replacement policies and the increase in sulfuric acid prices, and the prices of magnesium sulfate and magnesium oxide rose in the short term. It is recommended to stock up appropriately.

6)Calcium iodate

The price of refined iodine rose slightly, the supply of calcium iodate was tight, some iodide manufacturers were shut down or limited production, and the supply of iodide was tight. It is expected that the tone of a long-term steady and small increase in iodide will remain unchanged. It is recommended to stock up appropriately.

7)Sodium selenite

In terms of raw materials: The prices of non-ferrous metals have been continuously rising. The overall market for crude selenium and selenium dioxide has seen a decline in volume but stable prices. Before the festival, cautious stockpiling was carried out. The support from high-end demand is stronger than that from traditional sectors. Due to capital speculation, the upstream supply of crude selenium and selenium dioxide has not been reduced, leading to a shortage of raw materials. The inventory of manufacturers is low, and prices have risen. Buy on demand.

8)Cobalt chloride

Cobalt chloride prices are expected to remain high and stable in the short term, with some support below due to tight supply of raw materials and cost support, but sluggish demand limits upside potential.

9)Cobalt salt/potassium chloride/potassium carbonate/calcium formate/iodide

1. Cobalt: The trading atmosphere in the cobalt market has weakened, and spot prices have remained stable. On the supply side, supported by rising raw material costs, smelters’ quotations remained firm. Towards the end of the year, the purchasing intentions of downstream enterprises have generally weakened. Coupled with the gradual recovery of Congolese exports and the decline in electrolytic cobalt prices and other news factors suppressing market trading sentiment, enterprise purchasing has returned to rigid demand. With strong support from upstream raw material costs, it is expected that cobalt sulfate prices will still show a pattern of “more likely to rise than fall” in the short term.

2. Potassium chloride: There is a strong willingness to hold prices, an obvious reluctance to sell, and a low willingness to actively lower prices. The continuous implementation of national policies to ensure supply and stabilize prices has played a stabilizing role in market sentiment and has curbed the space for excessive price increases.

Outlook: In the short term, the price of potassium chloride is expected to remain at a high level with a narrow range of consolidation, and there may be small fluctuations in some varieties due to demand release or arrival. Prices are likely to remain high in March as spring plowing demand is released in a concentrated manner; Prices may pull back after April if domestic capacity recovers or policy reserves are released.

3. Domestic formic acid market prices will still face some downward pressure, and major producers have plans to limit formic acid production. The current stalemate in supply and demand in the market remains unchanged, and the pressure of inventory digestion still exists. It is necessary to pay attention to the changes in supply and demand in the market. Calcium formate prices may be slightly adjusted this week, and it is recommended to stock up according to demand.

4. Iodide prices are stable this week compared to last week.

Post time: Feb-27-2026