Trace Elements Market Analysis

I,Analysis of non-ferrous metals

Week-on-week: Month-on-month:

| Units | Week 3 of January | Week 4 of January | Week-on-week changes | December average price | Average price as of January 23 | Month-on-month changes | Current price on January 27 | |

| Shanghai Metals Market # Zinc ingots | Yuan/ton |

24580 |

24310 |

↓270 |

23070 |

24327 |

↑1257 |

24760 |

| Shanghai Metals Network # Electrolytic copper | Yuan/ton |

102818 |

100525 |

↓2293 |

93236 |

101782 |

↑8546 |

101370 |

| Shanghai Metals Australia

Mn46% manganese ore |

Yuan/ton |

42.15 |

42.15 |

- |

41.58 |

42.09 |

↑0.51 |

42.15 |

| The price of imported refined iodine by Business Society | Yuan/ton |

635000 |

635000 |

- |

635000 |

635000 |

- |

635000 |

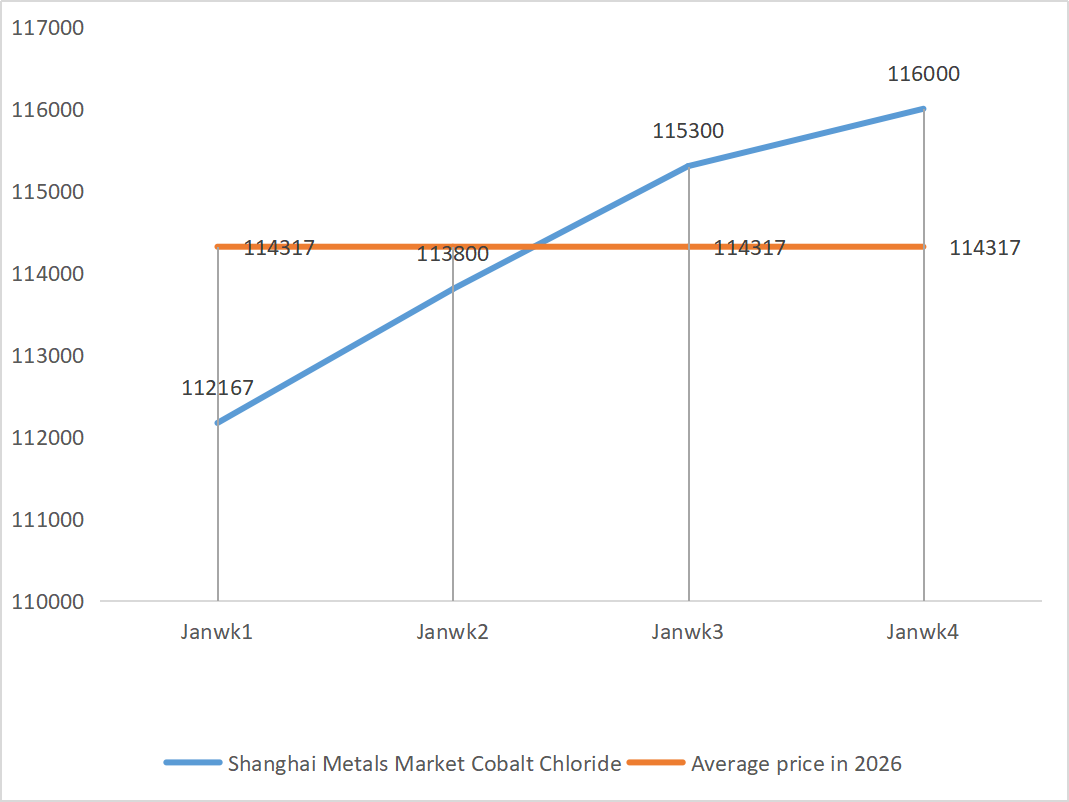

| Shanghai Metals Market Cobalt Chloride

(co≥24.2%) |

Yuan/ton |

115300 |

116000 |

↑700 |

109135 |

115033 |

↑5898 |

116000 |

| Shanghai Metals Market Selenium Dioxide | Yuan/kilogram |

125.5 |

136.5 |

↑11 |

112.9 |

128.17 |

↑15.27 |

132.5 |

| Capacity utilization rate of titanium dioxide manufacturers | % |

77.09 |

72.86 |

↓4.23 |

74.69 |

7593 |

↑1.24 |

1)Zinc sulfate

① Raw materials: Zinc hypooxide: The supply shortage situation has eased somewhat, but manufacturers’ quotations remain relatively firm, and the cost side of enterprises continues to be under pressure.

Zinc network price background: Geopolitical risks outside the United States still exist, and the interest rate decision and statement released by the Federal Reserve FOMC are mainly guiding information, which may affect market sentiment and thereby zinc prices; From a fundamental perspective, some downstream demand-side enterprises plan to take a holiday at the end of January and the beginning of February. It is expected that the operating rates of zinc ingot downstream galvanizing and die-casting zinc manufacturers will decline by 1 to 3 percent.

Overall, the fundamentals are unlikely to provide momentum, and zinc prices are expected to fluctuate around 24,500 yuan per ton next week.

② Sulfuric acid: Market prices are stable this week.

This week, producers’ operating rate was 68% (-11% compared to the previous week), and capacity utilization rate was 72% (+3% compared to the previous week). Supported by high prices of raw zinc and stable prices of sulfuric acid, the cost side of zinc sulfate was strongly supported. Overall demand remained solid. Zinc sulfate prices are expected to stabilize at high levels in the short term.

2)Manganese sulfate

Raw materials: ① Strong cost support: Tight manganese ore supply and firm price, while high sulfuric acid prices jointly support the cost side

② Sulfuric acid prices remain stable at a high level.

This week, producers’ operating rate was 67% (down 14% from the previous week), capacity utilization rate was 51% (down 8% from the previous week), and major producers’ orders were scheduled until mid to late February. Strong cost support: Tight manganese ore supply and firm prices, high sulfuric acid prices, together supporting the cost side, with strong support, manganese sulfate prices are expected to remain at a high and firm level.

Based on the analysis of enterprise order volume and raw material factors, manganese sulfate is expected to remain firm in the short term. Customers are advised to purchase according to their needs.

3)Ferrous sulfate

Raw materials: Obvious upstream constraints: High inventories in the titanium dioxide industry and off-season sales have led some manufacturers to suspend production; Significant diversion of raw materials: Stable demand in the lithium iron phosphate industry continues to divert raw material supply; Chain transmission: The discontinuation of the main product directly leads to a simultaneous reduction in the production of the by-product ferrous sulfate.

This week, the factory’s operating rate was 60%, down 20% from the previous week; Capacity utilization remained at 19 per cent, down 4 per cent from the previous week, with manufacturers’ capacity not fully unleashed and tight market supply remaining.

It is expected that in the medium to short term, the market will continue the pattern of “weak supply and strong demand”, and the price of ferrous sulfate will remain firm at a high level, supported by the slow recovery of capacity and the continued tightness of raw materials. Buy and stock up at the right time based on your own inventory situation.

4)Copper sulfate/basic copper chloride

Macroscopically, U.S. November PCE data rose moderately, in line with market expectations, but dampened optimism about a rate cut. In terms of fundamentals, copper and gold production in Mantoverde, Chile, is close to standstill, intensifying supply tightness; Imports are slightly replenished and domestic supply is stable, and overall supply remains relatively stable. Demand has picked up, driven by stabilized copper prices and Spring Festival stockpiling. In terms of inventories, copper inventories in major regions across the country rose by 2.9% month-on-month, but the accumulation rate slowed.

The copper market is in a game pattern of “macro pressure and strong fundamentals”, with bulls and bears checking each other. It is expected that the copper price will still fluctuate in the range of 100,000-102,000 yuan/ton next week, and the copper sulfate price will adjust along with the copper price fluctuations.

Customers are advised to take advantage of their inventories to stock up when copper prices fall back to a relatively low level, so as to ensure supply while controlling costs.

5)Magnesium sulfate/magnesium oxide

In terms of raw materials: Currently, sulfuric acid in the north is stable at a high level.

Magnesium oxide and magnesium sulfate prices have risen. The impact of magnesite resource control, quota restrictions and environmental rectification has led to many enterprises producing based on sales. Light-burned magnesium oxide enterprises shut down on Friday due to capacity replacement policies and the increase in sulfuric acid prices, and the prices of magnesium sulfate and magnesium oxide rose in the short term. It is recommended to stock up appropriately.

6)Calcium iodate

The price of refined iodine rose slightly, the supply of calcium iodate was tight, some iodide manufacturers were shut down or limited production, and the supply of iodide was tight. It is expected that the tone of a long-term steady and small increase in iodide will remain unchanged. It is recommended to stock up appropriately.

7)Sodium selenite

In terms of raw materials: The prices of non-ferrous metals continue to rise. The overall market for crude selenium and selenium dioxide is shrinking in volume but stable in price. Pre-holiday stockpiling is cautious. The support from high-end demand is stronger than that in traditional fields. Capital speculation leads to a shortage of raw materials due to the upstream non-shipment of crude selenium and selenium dioxide. The inventory of manufacturers is low and the price is raised. Buy on demand.

8)Cobalt chloride

The current cobalt chloride market presents a situation of “stable production, sufficient orders and cost support”. Manufacturers’ quotations remain stable and mainstream orders are scheduled until the first half of February. With no significant fluctuations in raw material prices and a moderate recovery in downstream demand, prices are expected to remain stable in the short term.

Cobalt chloride prices are expected to remain stable at a high level, more likely to rise than fall, under the combined effect of heightened expectations of raw material shortages and seasonal recovery of downstream demand.

9)Cobalt salts/potassium chloride/potassium carbonate/calcium formate/iodide

1. Cobalt: The trading atmosphere in the cobalt market has weakened, and spot prices have remained stable. On the supply side, supported by rising raw material costs, smelters’ quotations remained firm. Towards the end of the year, the purchasing intentions of downstream enterprises have generally weakened. Coupled with the gradual recovery of Congolese exports and the decline in electrolytic cobalt prices and other news factors suppressing market trading sentiment, enterprise purchasing has returned to rigid demand. With strong support from upstream raw material costs, it is expected that cobalt sulfate prices will still show a pattern of “more likely to rise than fall” in the short term.

2. Potassium chloride: Compared with last week, the increase in potassium chloride prices is not too significant, and there are many cases of holding back sales and stopping sales. Processed potassium sulfate plants raised prices, but downstream demand was limited. The abnormal movement of potassium fertilizer has drawn attention from relevant authorities. It is recommended to pay attention to the quantity of stocks in Hong Kong and the international environment, and to make appropriate preparations and replenish purchases as needed in the near future.

3. The stalemate in supply and demand in the formic acid market remains unchanged. There is considerable pressure to digest the inventory. Downstream demand is unlikely to show substantial improvement in the short term. In the short term, prices will still be mainly fluctuating and weak. Calcium formate demand is average. It is recommended to pay attention to the formic acid market and purchase as needed

4. Iodide prices remained stable this week compared to last week.

Post time: Jan-29-2026