Trace Elements Market Analysis

I,Analysis of non-ferrous metals

Week-on-week: Month-on-month:

| Units | Week 5 of April | Week 1 of May | Week-on-week changes | April average price | The average price up to May 8 | Month-on-month changes | Current price May 13 | |

| Shanghai Metals Market # Zinc ingots | Yuan/ton |

23800 |

24067 |

↑267 |

23727 |

24067 |

↑340 |

24710 |

| Shanghai Metals Network # Electrolytic copper | Yuan/ton |

102003 |

102717 |

↑714 |

100316 |

102717 |

↑2401 |

108500 |

| Shanghai Metals Australia

Mn46% manganese ore |

Yuan/ton |

45.11 |

42.25 |

- |

45.09 |

42.25 |

↓2.84 |

44.25 |

| Business Society imported refined iodine prices | Yuan/ton |

635000 |

635000 |

- |

635000 |

635000 |

- |

635000 |

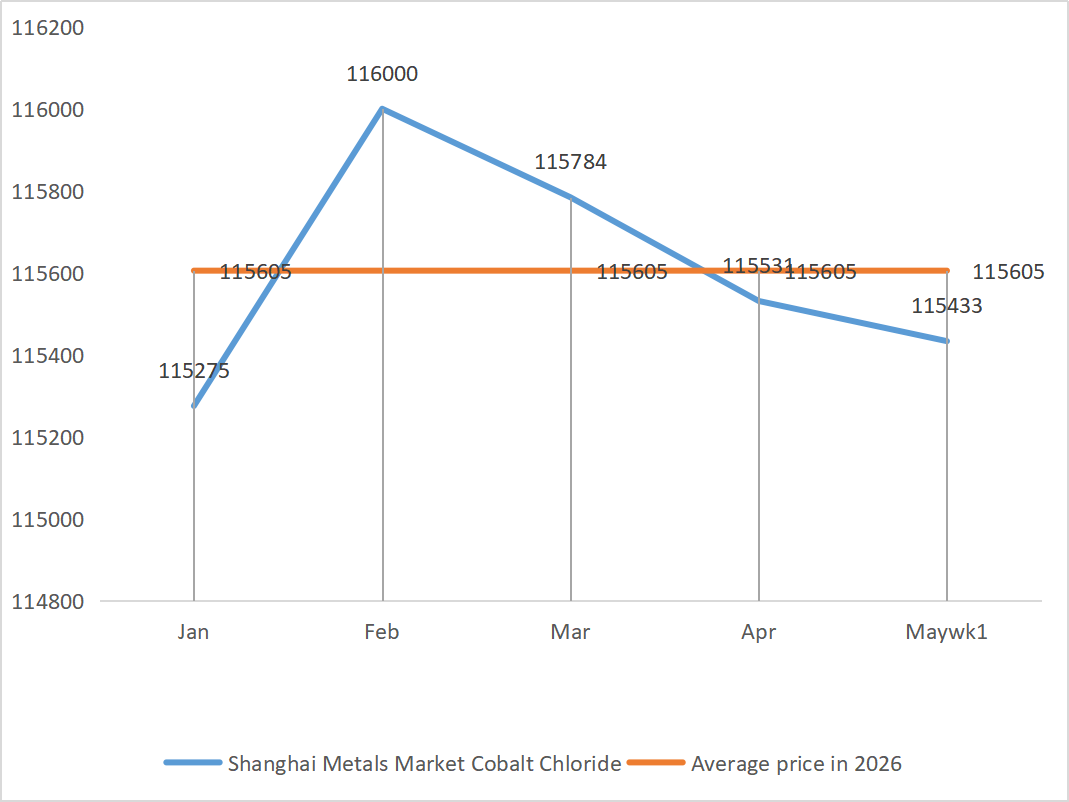

| Shanghai Metals Market Cobalt Chloride

(co≥24.2%) |

Yuan/ton |

115350 |

115433 |

- |

115531 |

115433 |

↓98 |

115500 |

| Shanghai Metals Market Selenium Dioxide | Yuan/kilogram |

172.5 |

172.5 |

- |

172.50 |

172.50 |

- |

172.5 |

| Capacity utilization rate of titanium dioxide manufacturers | % |

74.22 |

76.16 |

- |

71.78 |

76.16 |

↑4.48 |

1)Zinc sulfate

① Raw materials: Zinc hypooxide: The transaction coefficient remains high.

Zinc network price background: Macro: Resurgence of US-Iran conflict + Continuation of geopolitical risks + strengthening of the US dollar index → bearish for zinc prices; Fundamentals: Zinc concentrate processing fees fall to $950 per ton (the lowest in nearly three years) + low LME zinc inventories (19,500 tons in the past month, a 17% drop), providing bottom support for prices. Forecast: The average price of zinc next week will be 24,200 yuan per ton.

② Sulfuric acid: High price this week.Based on the analysis of raw materials and upstream orders, zinc sulfate is expected to remain strong in the short term.

2)Manganese sulfate

① The price of sulfuric acid is high and firm.

Manganese sulfate was quoted at a high price this week, mainly due to the continuous increase in prices of various raw materials. Currently, the overall operating rate is not high, resulting in cost hikes.

Delivery is tight. Customers are advised to lock in orders in a timely manner based on inventory to avoid the peak delivery period

3)Ferrous sulfate

The capacity utilization rate of titanium dioxide producers at the raw material end has slightly rebounded, but ferrous heptahydrate has been significantly affected by cross-industry diversion in the lithium iron phosphate industry, and the inflow of ferrous monohydrate has increased limited, and the tight situation remains unchanged.

Sulfuric acid: High for the week.

Taking into account recent corporate inventories and upstream operating rates, ferrous sulfate is expected to rise in the short term. Customers are advised to increase their inventories appropriately.

4)Copper sulfate/basic copper chloride

Weaker US dollar index combined with news of delayed copper mine resumption in Indonesia intensifying expectations of supply tightening, frequent disruptions at the mine end, acid shortages combined with a significant reduction in domestic inventories supported copper prices. The geopolitical conflict pushed up oil prices and inflation expectations, and the strong performance of global stock markets, especially U.S. technology stocks, further highlighted the appeal of AI computing infrastructure, which was positive for copper prices. Delays in copper mine resumption in Indonesia, sulfuric acid shortages and domestic inventory reduction have consolidated the supply shortage.

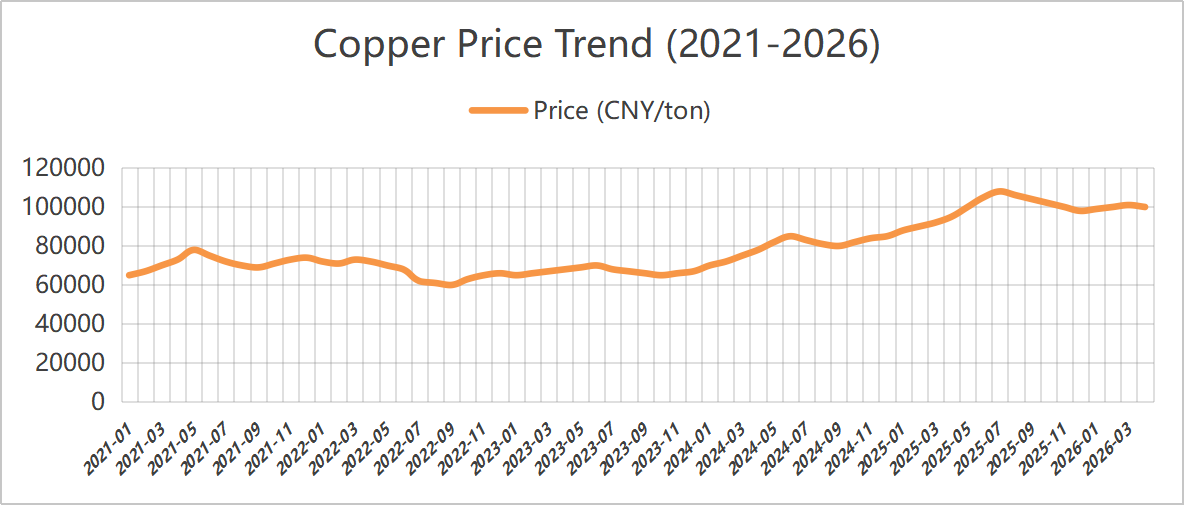

1) Current price trend

Subsequently, it is necessary to pay attention to the expected trends after several macro events in May are implemented, including the US-Iran negotiations, Trump's visit to China and the power transition of the Federal Reserve. Copper prices may test previous highs, while closely watching the actual feedback from the spot market. It is expected that the main operating range of Shanghai copper will be around 106,200-109,200 yuan per ton in the near future.

2) Copper price trend over the past five years (2021-2026) : Summary of the five-year trend: Upward - pullback - sideways - breakout again - High consolidation. It is currently at its highest point in nearly five years.

5) Magnesium sulfate/magnesium oxide

In terms of raw materials: Currently, sulfuric acid in the north is stable at a high level.

Due to the post-holiday control of magnesite resources, quota restrictions and environmental rectification, many enterprises are producing based on sales. Light-burned magnesia enterprises have been forced to suspend production for transformation due to capacity replacement policies, and short-term productivity is unlikely to increase significantly. Due to the war, sulfur prices rose and sulfuric acid prices went up, providing favorable support for magnesium sulfate prices. It is recommended to stock up appropriately.

6)Calcium iodate

The feed-grade calcium iodate market has remained stable at high levels and fluctuated narrowly over the past week. Raw iodine prices were stable and cost support was strong. Manufacturers operate normally, supply is stable, downstream feed enterprises purchase on demand, demand is moderately released, short-term stability is maintained without obvious ups and downs to drive. It is recommended to stock up appropriately.

7)Sodium selenite

In terms of raw materials: Crude selenium and selenium dioxide are generally weak and volatile. The supply of by-products from smelting is loose, while the demand for glass and feed downstream is weak, and the transaction volume is low. Raw material costs support the decline is limited, and it is expected to maintain a weak range in the short term. Sodium selenite raw material costs have decreased, and speculation has withdrawn from the price decline

8)Cobalt chloride

Cobalt sulfate and cobalt chloride have stopped falling and are trading sideways. The tightening of cobalt quotas in Congo has propped up raw material costs. Downstream strong demand has led to flat transactions. Lithium batteries are gradually resuming production. Short-term cobalt salts are expected to be stable with a slight upward trend. It is recommended to purchase on demand.

9)Potassium chloride/potassium carbonate/calcium formate/iodide

1.Potassium chloride: A small increase in potassium fertilizer. During the off-season for potash demand, factors restricting the increase: off-season for demand, policy constraints, weak downstream, pay attention to domestic and international environmental factors, stock up appropriately as needed.

2.Formic acid prices continue to fall, production enterprises have a large amount of inventory, and demand is weak. Calcium formate prices are falling as costs are reduced. It is recommended to stock up based on demand.

3. Iodide prices remained stable this week compared to last week.

Free consultation

Request samples

Contact Us

Post time: May-14-2026