Trace Elements Market Analysis

I,Analysis of non-ferrous metals

Week-on-week: Month-on-month:

| Units | Week 2 of August | Week 3 of August | Week-on-week changes | Average price in July | As of August 22Average price | Month-on-month change | Current price as of August 26 | |

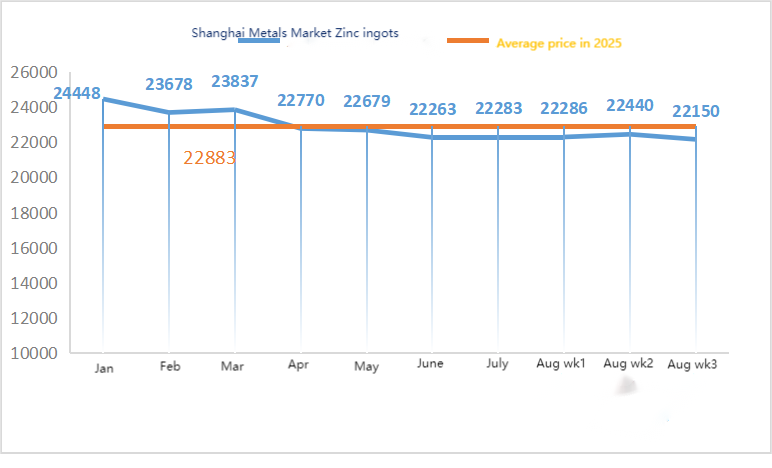

| Shanghai Metals Market # Zinc ingots | Yuan/ton |

22440 |

22150 |

↓290 |

22356 |

22288 |

↓68 |

22280 |

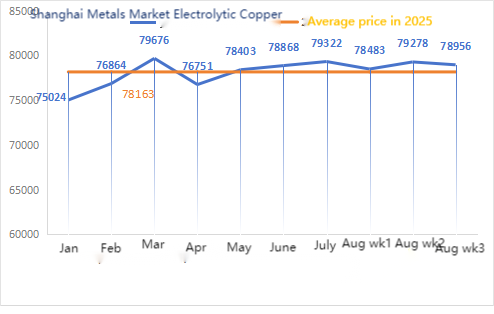

| Shanghai Metals Market # Electrolytic Copper | Yuan/ton |

79278 |

78956 |

↓322 |

79322 |

78870 |

↓452 |

79585 |

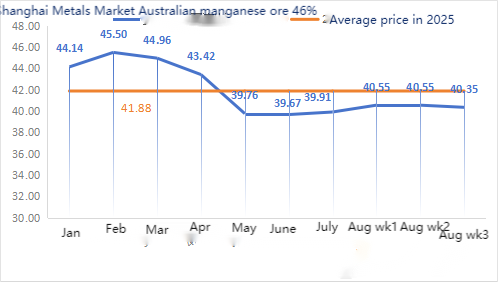

| Shanghai Metals AustraliaMn46% manganese ore | Yuan/ton |

40.55 |

40.35 |

↓0.2 |

39.91 |

40.49 |

↑0.58 |

40.15 |

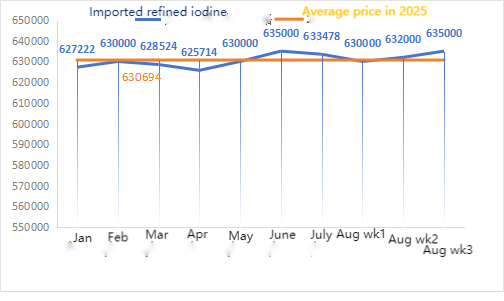

| The price of imported refined iodine by Business Society | Yuan/ton |

632000 |

635000 |

↑3000 |

633478 |

632189 |

↓1289 |

635000 |

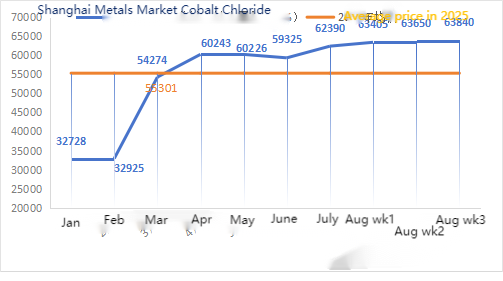

| Shanghai Metals Market Cobalt Chloride(co≥24.2%) | Yuan/ton |

63650 |

63840 |

↑190 |

62390 |

63597 |

↑1207 |

64250 |

| Shanghai Metals Market Selenium Dioxide | Yuan/kilogram |

96.8 |

99.2 |

↑2.4 |

93.37 |

96.25 |

↑2.88 |

100 |

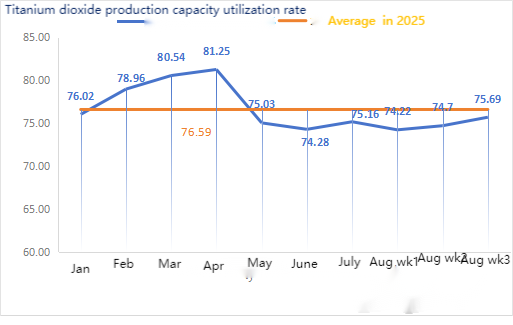

| Capacity utilization rate of titanium dioxide manufacturers | % |

74.7 |

75.69 |

↑0.99 |

75.16 |

74.53 |

↓0.63 |

In terms of raw materials: zinc hypooxide: With high raw material costs and strong purchasing intentions from downstream industries, manufacturers have a strong willingness to raise prices, and the high transaction coefficient is constantly being refreshed. ② Sulfuric acid prices remained stable across the country this week. Soda ash: Prices were stable this week. ③ Macroscopically, expectations of Fed rate cuts are fluctuating, the dollar index is rising, non-ferrous metals are under pressure, and the market is concerned about the outlook for zinc demand. In terms of fundamentals, domestic inventories continue to rise, the pattern of zinc surplus remains unchanged, and consumption is still weak at present. Macro sentiment fluctuates, the center of gravity of Shanghai zinc is moving down, awaiting more macro guidance.

Zinc prices are expected to run in the range of 22,000 to 22,500 yuan per ton next week.

The operating rate of the water sulfate zinc sample factory on Monday was 83%, down 11% from the previous week, and the capacity utilization rate was 71%, down 2% from the previous week. The quotations for this week are the same as last week. In the first ten days of the week, customers in the feed and fertilizer industries had stockpiling, with major manufacturers scheduling orders until mid-September and some until late September. The overall upstream operating rate was normal, but the order intake was significantly insufficient. There are various levels of pullbacks in the spot market. Feed enterprises have not been very active in purchasing recently. Under the dual pressure of upstream enterprises’ operating rates and insufficient existing orders, zinc sulfate will continue to operate weakly and stably in the short term. It is suggested that the demand side determine the purchasing plan in advance based on their own inventory situation.

In terms of raw materials: ① The manganese ore market was stable with fluctuations and a pullback. Among them, the prices of northern Hong Kong and Macau blocks, Gabon blocks, etc. dropped slightly by 0.5 yuan per ton, while the prices of other types of ore remained stable for the time being. The manganese ore market as a whole remained stable and in a wait-and-see mode. There were few quotations from traders and few inquiries from factories. The manganese ore price was in a stalemate where low prices were hard to inquire about and high prices were hard to sell. The trading atmosphere at the port was sluggish. The recovery of coking coal sentiment has driven the silicon manganese market to rise in resonance. At present, alloy factories and terminal steel mills are operating at a relatively high level, providing strong support for the demand side of raw material manganese ore. Mainstream miners expect a new round of inventory replenishment demand in September and have a low willingness to sell at low prices. The price difference between factory inquiries and traders’ quotations has widened.

② Sulfuric acid prices are mainly stable.

This week, the operating rate of manganese sulfate sample manufacturers was 71%, a 15% decrease compared to the previous week. Capacity utilization rate was 44%, down 17% from the previous week. Some factories’ maintenance led to a decline in data. Factories’ delivery was tight. Quotations from mainstream factories rose this week compared with last week. In the second half of the month, the number of manganese sulfate manufacturers shut down for maintenance increased. There was no significant increase in foreign trade orders, and domestic end customers were not very enthusiastic about replenishing inventories. Based on the analysis of enterprise order volume and raw material factors, manganese sulfate will remain stable in the short term. It is recommended that customers appropriately reduce inventory.

It is recommended that the demand side determine the purchase plan in advance based on its own inventory situation.

In terms of raw materials: Downstream demand for titanium dioxide remains sluggish. Some manufacturers have accumulated titanium dioxide inventories, resulting in low operating rates. The tight supply situation of ferrous sulfate in Qishui continues.

This week, the operating rate of sample ferrous sulfate manufacturers was 75%, and the capacity utilization rate was 24%, remaining flat compared with the previous week. Quotations this week were stable compared to last week. With producers scheduling orders until mid-October, the supply of raw material ferrous heptahydrate is tight and the price remains firm at a high level. With cost support and relatively abundant orders, it is expected that the price of ferrous monohydrate will remain firm at a high level in the later period, mainly affected by the operating rate of the titanium dioxide industry and the relative progress of raw material supply. Recently, the shipment of ferrous sulfate heptahydrate has been good, which has led to rising costs for ferrous sulfate monohydrate producers. Currently, the overall operating rate of ferrous sulfate in China is not good, and enterprises have very little spot inventory. Ferrous sulfate is expected to rise in the short term, and customers are advised to increase their inventories appropriately.

4)Copper sulfate/basic copper chloride

Raw materials: Macroscopically, policy divergence within the Fed has emerged. While rates remained unchanged at the July meeting, a few officials have supported a rate cut in September. The market awaits news of the Ukraine talks, and the rebound in crude oil combined with strengthened expectations of a Fed rate cut is a positive support for copper prices.

In terms of fundamentals, the supply side has seen a clear shift from tight to loose spot supply of electrolytic copper due to increased arrivals from domestic refineries. The demand side is still in the traditional off-season, with downstream maintaining on-demand purchasing and replenishing inventories at low prices, and the overall sentiment is cautious. Overall, the positive macro outlook has provided some support for copper prices.

In terms of etching solution: Some upstream raw material manufacturers are deep processing etching solution, the raw material shortage is further intensified, and the transaction coefficient remains high.

In terms of price, it is expected that the copper net price will fluctuate narrowly within the range of 79,500 yuan per ton this week.

This week, the operating rate of copper sulfate/caustic copper producers is 100% and the capacity utilization rate is 45%, remaining flat compared with the previous week. This week, quotations from major manufacturers remained the same as last week.

Based on the recent trend of raw materials and the operating conditions of manufacturers, copper sulfate is expected to remain at a high level with fluctuations in the short term. Customers are advised to maintain normal inventories.

Raw materials: The raw material magnesite is stable.

The factory is operating normally and production is normal. The delivery time is generally around 3 to 7 days. Prices have been stable from August to September. As winter approaches, there are policies in major factory areas that prohibit the use of kilns for magnesium oxide production, and the cost of using fuel coal increases in winter. Combined with the above, it is expected that the price of magnesium oxide will rise from October to December. Customers are advised to purchase based on demand.

In terms of raw materials: Currently, the price of sulfuric acid in the north is on the rise in the short term.

Magnesium sulfate plants are operating at 100%, production and delivery are normal, and orders are scheduled until early September. The price of magnesium sulfate is expected to remain stable in August. As September approaches, the price of sulfuric acid may rise, and it is not ruled out that the price of magnesium sulfate will increase further. Customers are advised to purchase according to their production plans and inventory requirements.

Raw materials: The domestic iodine market is stable at present, the supply of imported refined iodine from Chile is stable, and the production of iodide manufacturers is stable.

This week, the production rate of calcium iodate sample manufacturers was 100%, the capacity utilization rate was 36%, the same as the previous week, and the quotations of mainstream manufacturers remained stable. The livestock and poultry industry saw a rebound in demand as the weather turned cooler, and aquatic feed manufacturers were in the peak demand season, driving a slight increase in demand this week compared to the normal week.

Demand remained stable this week compared to the normal week. Customers are advised to purchase on demand based on production planning and inventory requirements.

In terms of raw materials: The auction price of crude selenium from copper smelters has been rising recently, demonstrating the increasing activity of selenium market transactions and the growing overall confidence in the future trend of selenium market prices.

This week, the operating rate of sodium selenite sample manufacturers was 100% and the capacity utilization rate was 36%, remaining flat compared with the previous week. Affected by the increase in export orders from manufacturers, the price of pure sodium selenite powder rose this week compared with last week.

Raw material prices are still expected to rise, and demand is advised to purchase at the right time based on their own inventories.

Raw materials: On the supply side, upstream smelters continue to be bullish on cobalt products, and with the consumption of raw materials and cobalt chloride, the sentiment of hoarding and holding back sales is intensifying; On the demand side, due to the continuous price hikes in recent times, there has been a growing wait-and-see sentiment downstream. Prices are expected to rise slightly next week.

As the weather gradually cools down, rumination feed intake and demand have picked up, maintaining essential purchases. Demand increased slightly this week compared to the normal week.

The price of cobalt chloride feedstock is not ruled out to rise further. Customers are advised to purchase at the right time based on inventory.

10)Cobalt salt/potassium chloride/potassium carbonate/calcium formate/iodide

1 Cobalt salt prices are affected by the ban on cobalt exports in the Democratic Republic of the Congo, with tight supply of raw materials and obvious cost support. In the short term, cobalt salt prices are likely to remain volatile and upward. Due to the continuous increase in costs, smelting enterprises will maintain price support and basically suspend quotations for individual orders. After domestic prices stabilized, traders postponed selling at a lower price and raised their quotations slightly. Subsequent price changes should focus on rising costs and actual purchases by downstream customers after the summer break ends in late August and early September.

2. The domestic market price of potassium chloride remains stable with a slight loosening, and the demand has weakened temporarily

Although traders’ quotations have remained stable for the time being, some traders’ willingness to sell has increased, driving sales to rise slightly. Overall, under the influence of enhanced import expectations , the high-end price of potash fertilizer may loosen slightly in the short term, but constrained by factors such as maintenance and production cuts, the adjustment of is expected to be limited . It is expected to fluctuate in a narrow range of , with a low possibility of significant ups and downs. The price of potassium carbonate follows the price of potassium chloride.

3. Calcium formate prices remained stable at high levels this week. The price of raw formic acid rose as factories shut down for maintenance. Some calcium formate plants have stopped taking orders.

4. Iodide prices remained stable this week compared to last week.

Post time: Aug-29-2025