race Elements Market Analysis

I,Analysis of non-ferrous metals

Week-on-week: Month-on-month:

| Units | Week 5 of July | Week 1 of August | Week-on-week changes | Average price in July | As of August 8

Average price |

Month-on-month change | Current price as of August 12 | |

| Shanghai Metals Market # Zinc ingots | Yuan/ton |

22430 |

22286 |

↓144 |

22356 |

22277 |

↓79 |

22500 |

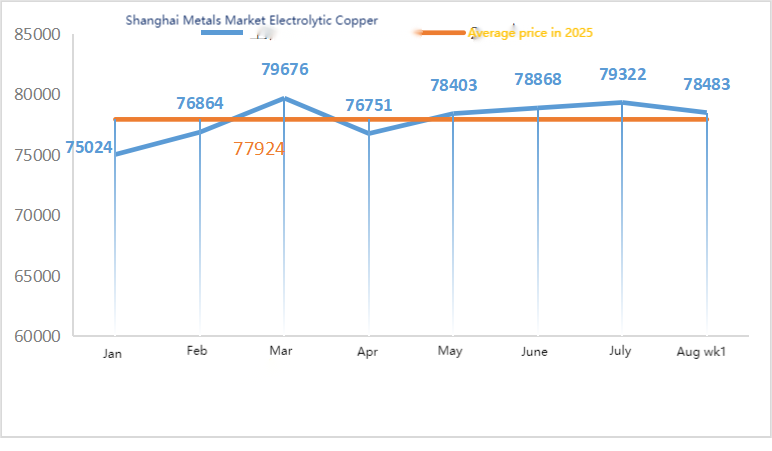

| Shanghai Metals Market # Electrolytic Copper | Yuan/ton |

78856 |

78483 |

↓373 |

79322 |

78458 |

↓864 |

79150 |

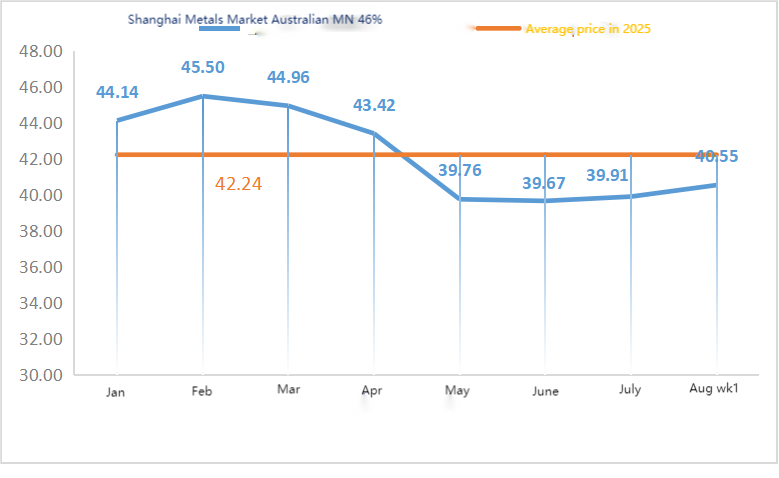

| Shanghai Metals Australia

Mn46% manganese ore |

Yuan/ton |

40.33 |

40.55 |

↑0.22 |

39.91 |

40.55 |

↑0.64 |

40.55 |

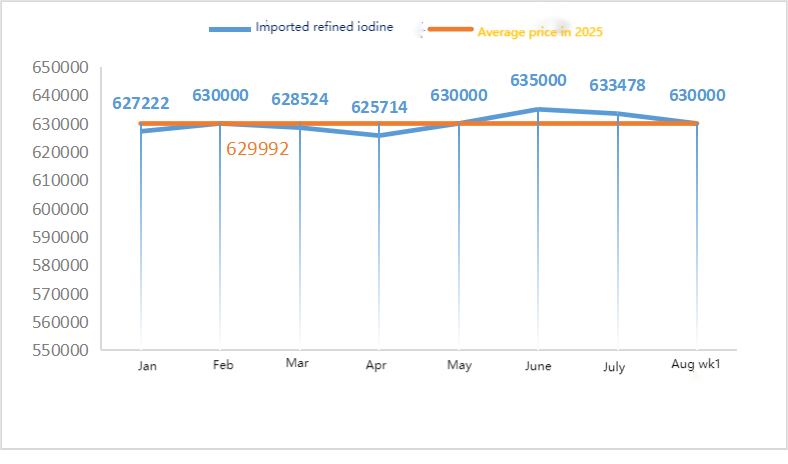

| The price of imported refined iodine by Business Society | Yuan/ton |

63000 |

63000 |

633478 |

630000 |

↓3478 |

630000 |

|

| Shanghai Metals Market Cobalt Chloride

(co≥24.2%) |

Yuan/ton |

62915 |

63405 |

↑490 |

62390 |

63075 |

↑685 |

63650 |

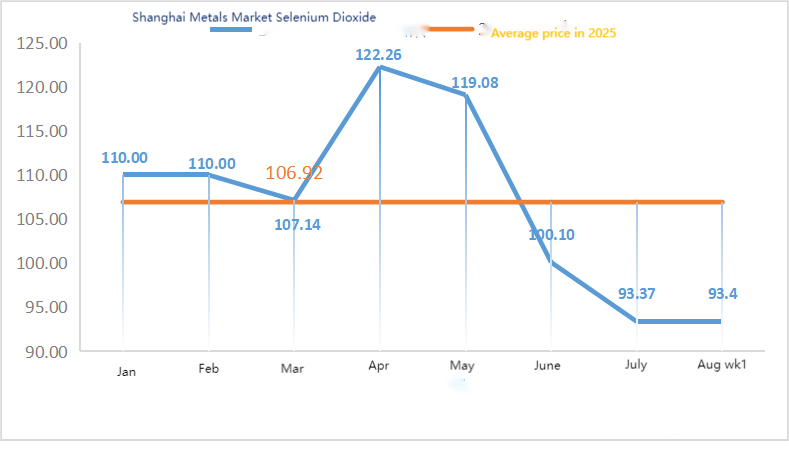

| Shanghai Metals Market Selenium Dioxide | Yuan/kilogram |

91.2 |

93.4 |

↑2.2 |

93.37 |

93.33 |

↓0.04 |

95 |

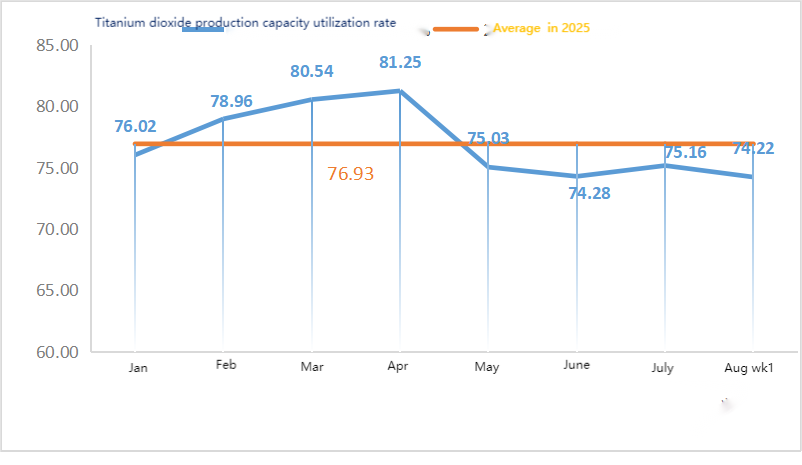

| Capacity utilization rate of titanium dioxide manufacturers | % |

73.52 |

74.22 |

↓0.7 |

75.16 |

73.87 |

↓1.29 |

Raw materials: Zinc hypooxide: With high raw material costs and strong purchasing intentions from downstream industries, the transaction coefficient remained the same as last week, and the post-holiday highs were constantly being refreshed. ② Sulfuric acid prices remained stable across the country this week. Soda ash: Prices were stable this week. ③ On the macro front, Fed Daly said the timing of rate cuts is near and there is a greater likelihood of more than two rate cuts this year. Goldman Sachs expects the Fed to cut rates by 25 basis points three times in a row starting from September and suggests a 50 basis point cut if the unemployment rate rises, boosting metal prices. In terms of fundamentals, the pattern of strong supply and weak demand remains unchanged, the off-season feature of demand continues, and downstream essential purchases are dominant.

On Monday, the operating rate of water zinc sulfate sample manufacturers was 94%, up 11% from the previous week, and the capacity utilization rate was 73%, up 5% from the previous week. Against the backdrop of abundant orders from mainstream manufacturers, quotations rose this week compared with last week. With major manufacturers scheduling orders until early September and firm raw material costs, it is not ruled out that prices will rise further. Demand is advised to determine their purchasing plans in advance based on their inventory situation.

Zinc prices are expected to run in the range of 22,500 to 23,000 yuan per ton.

In terms of raw materials: ① The operating rates of downstream alloy factories in the north and south are stable. Most alloy factories maintain essential purchasing and there is no phenomenon of large stockpiling. The demand for manganese ore remains stable and the mentality of price reduction still exists.

② Sulfuric acid prices remained stable this week.

This week, the operating rate of sample manufacturers of manganese sulfate was 86% and the capacity utilization rate was 61%, remaining flat compared with the previous week. Quotations from mainstream manufacturers remained stable this week compared with last week. The peak season for aquaculture in the south provided some support for manganese sulfate demand, but the overall demand boost was limited. Driven by the maintenance information from some manufacturers and the recent changes in freight conditions, the demand side is concerned about tight delivery in the future, and the purchasing enthusiasm has picked up. Demand this week is stable compared with the normal week.

The raw material cost support for manganese sulfate quotations is relatively strong, and the price is relatively firm. It is recommended that the demand side purchase and stock up at an appropriate time based on the production situation.

In terms of raw materials: Downstream demand for titanium dioxide remains sluggish. Some manufacturers have accumulated titanium dioxide inventories, resulting in low operating rates. The tight supply situation of ferrous sulfate in Qishui continues.

This week, the operating rate of sample ferrous sulfate manufacturers was 75%, and the capacity utilization rate was 24%, remaining flat compared with the previous week. Quotations this week were stable compared to last week. With cost support and relatively abundant orders, ferrous sulfate is firm, mainly due to the relative progress of raw material supply affected by the operating rate of the titanium dioxide industry. Recently, the shipment of heptahydrate ferrous sulfate has been good, which has led to an increase in costs for monohydrate ferrous sulfate producers. Currently, the overall operating rate of ferrous sulfate in China is not good, and enterprises have very little spot inventory, which brings favorable factors for the price increase of ferrous sulfate. At present, orders from mainstream factories are scheduled until mid-September, and prices are expected to rise in the short term. It is recommended that customers increase their inventories appropriately.

4)Copper sulfate/basic copper chloride

Raw materials: On a macro level, enhanced expectations of Fed rate cuts have boosted copper prices. Boosted by the consensus reached between China and the US on the continued suspension of the 24% tariff, which outweighed the pressure from increased supply and a stronger dollar.

In terms of fundamentals, there is a pattern of weak supply and demand

Etching solution: Some upstream raw material manufacturers have deep processing of etching solution, further intensifying the raw material shortage, and the transaction coefficient remains high.

In terms of price, there is still uncertainty on the macro level. Coupled with weak supply and demand on the fundamentals, it is expected that the copper net price will run in the range of 78,500-79,500 yuan per ton this week. Copper sulfate producers are operating at 100% this week, with capacity utilization at 45%, remaining flat compared to the previous week. Due to the recent high temperatures, copper sulfate/caustic copper producers have been relatively tight with raw materials recently, and the order volume has basically remained at around half a month. Based on the recent trend of raw materials and the operating conditions of manufacturers, copper sulfate is expected to remain at a high level with fluctuations in the short term. It is recommended that customers maintain normal inventories.

Raw materials: The raw material magnesite is stable.

The factory is operating normally and production is normal. The delivery time is generally around 3 to 7 days. Prices have been stable from August to September. As winter approaches, there are policies in major factory areas that prohibit the use of kilns for magnesium oxide production, and the cost of using fuel coal increases in winter. Combined with the above, it is expected that the price of magnesium oxide will rise from October to December. Customers are advised to purchase based on demand.

Raw materials: The price of sulfuric acid in the north is currently rising in the short term.

Magnesium sulfate plants are operating at 100%, production and delivery are normal, and orders are scheduled until early September. The price of magnesium sulfate is expected to be stable with an upward trend in August. Customers are advised to purchase according to their production plans and inventory requirements.

In terms of raw materials: Currently, the domestic iodine market is operating stably. The arrival volume of imported refined iodine from Chile is stable, and the production of iodide manufacturers is stable.

This week, the production rate of calcium iodate sample manufacturers was 100%, the capacity utilization rate was 36%, the same as the previous week, and the quotations of mainstream manufacturers remained stable. The summer heat led to a decline in livestock feed, and manufacturers mostly purchased on demand. Aquatic feed manufacturers are in the peak demand season, driving up the demand for calcium iodate. This week’s demand is more stable than normal. Customers are advised to purchase according to their production plans and inventory requirements.

In terms of raw materials: Crude selenium resources became tight in late July and early August, far exceeding market expectations. The rebound in crude selenium prices partly reflects the recovery of the selenium dioxide market. Whether the peak season at the terminal will come earlier remains to be seen, but market confidence is beginning to strengthen.

This week, sample manufacturers of sodium selenite were operating at 100%, capacity utilization at 36%, flat compared with the previous week, and quotations from mainstream manufacturers remained stable. The cost of raw materials has strengthened support, and it is expected that prices will rise later. It is recommended that the demand side purchase according to its own inventory.

In terms of raw materials: Upstream smelters on the supply side have recently stepped up the pace of raw material procurement to ensure supply for downstream demand, but are bullish on the long-term future, so the shipment mentality is relatively calm. On the demand side, downstream purchasing sentiment has reversed recently. In the short term, cobalt chloride prices are expected to fluctuate.

This week, the cobalt chloride sample factory’s operating rate was 100%, and the capacity utilization rate was 44%, remaining flat compared with the previous week. Manufacturers’ quotations remained stable this week.

Cobalt chloride prices are relatively stable. Customers are advised to make purchases based on inventory.

10)Cobalt salts/potassium chloride/potassium carbonate/calcium formate/iodide

1. Mainstream enterprises’ raw materials are guaranteed by long-term orders, costs push prices stronger, downstream rigid purchases are dominant, zero orders transactions are sluggish. Overall market trading is sluggish, with some manufacturers relying on agreement orders to maintain production. Cobalt salt prices are expected to remain stable in the short term.

2. The domestic potassium chloride market continues to be tight in supply and firm in price. Although the operating rate of domestic potassium plants has rebounded, the supply mainly flows to compound fertilizer factories, and the market circulation volume is relatively small. The volume of imported potassium arriving at ports is limited, traders’ inventories are low, local quotations have risen slightly, but high-price deals are weak. Downstream demand was cautious, the market was in a wait-and-see mood, overall trading was light, and prices remained at a high level. In the short term, the contradiction between supply and demand remains, and the market is expected to remain firm. The price of potassium carbonate has been raised this week, affected by the price of raw material potassium chloride.

3. The price of calcium formate continued to rise this week. The price of raw formic acid rose as factories shut down for maintenance. Some calcium formate plants have stopped taking orders.

4. Iodide prices were stable and stronger this week compared to last week.

Post time: Aug-13-2025